Unicorn Investing: Private Assets

As my phone rang, it was an acquaintance, Mike. He wanted to know if we could beat a “low risk, low volatility investment producing 8% to 15% per year.”

I thought he was joking. It became apparent he was serious as he repeated a sales pitch for private equity and credit investments I heard recently.

I told Mike it was doubtful we could produce such claimed returns and unlikely anyone could.

Mike became flustered as he was sure it was more than a slick sales pitch.

To help Mike analyze the offer, I asked if he understood the deal structure on private equity or credit. He admitted he didn’t, beyond the enticing projected returns.

How do you derive a low risk 8% return when the 10-year US Treasury yields less than 4.5%? That is nearly 80% greater return. If the stock market averages 10% per year, how will you generate private equity returns that are 50% higher?

To potentially generate returns like this, there is either a duration mismatch (tie up money longer) or a credit mismatch (invest in something much lower quality). Or there is significant borrowed money inside, increasing risk and volatility.

Private assets are a combination of these which is eerily reminiscent of 2006 when things were sold as AAA credit, but were a mix of questionable assets made to look pretty.

Mike went on the offensive stating this was a “private” deal.

“Private” is mentioned as a benefit or exclusive club. It is the opposite. If they are calling you, the easy money has already been made. You forgo daily liquidity from publicly traded securities. Private equity deals often require you to sit for many years before a portion of liquidity is returned. Liquidity is often 5% per quarter.

Recognizing this, Oaktree Capital Co-CEO Robert O’Leary recently said in a nervous market private credit investors are already demanding liquidity. They are willing to take 90 cents on the dollar, going as low as the 50-cent range. That does not sound like my definition of “low risk.”

Confirming O’Leary’s comments, a Bain survey determined 63% of investors wanted P-E firms to exit, even at a discount.

Finally, I asked Mike if this is such a great deal, why are they selling it to you versus keeping it for themselves?

This caused Mike to stop and ask, “Why?”

As with most things in life, if you follow the money, you identify motivations and conflicts of interest.

Private deals remain the biggest fee generators for Wall Street banks.

Research by Richard Ennis, published in the Journal of Portfolio Management, concluded private market investments incur costs and fees of 5% to 8% per year. Ennis states, “This implies a near-insurmountable hurdle for these assets to generate excess returns.”

Additionally, Bain & Co. says Wall Street private equity firms are sitting on a record 29,000 companies they desperately want to sell. The average holding period for these private deals is now 6.7 years. Given this, clients are less willing to allocate more money to illiquid private deals as buyout fundraising fell by nearly 25% last year.

Mike still wanted his unicorn as he cited supposed private equity returns over time.

I asked Mike, “How do you know those are the returns if they weren’t sold and there isn’t a public market offering real-time quotes?”

In many cases, valuations from private equity firms have tremendous variance in their valuations and no real buyer or seller. Even if past private deals produced respectable returns, the future looks considerably more modest.

Again, Mike asked, “Why?”

The answer is simple. Private deals are structured with increasing amounts of debt. Ten years ago, debt was easy to obtain at very attractive levels. This significantly boosted returns.

Now these private companies have been passed around with greater leverage at each successive turn. However, the cost of borrowing is much higher now.

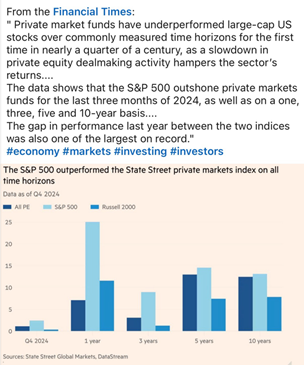

The result is lower returns. According to McKinsey & Co. analysis, private equity returns declined to roughly 3.8% in 2024. Worse yet, research from State Street and DataStream, published in the Financial Times, indicates private market funds actually underperformed the S&P 500 over the last one, three, five and ten years.

Furthermore, higher debt levels ultimately make any endeavor much riskier. For this reason, private equity firms are attempting to sell their assets to a brand-new target market…. the retail investor, the average person.

Buyer beware. If it sounds too good, it usually is. Unicorns only exist in fairy tales.

Dave Sather is a Certified Financial Planner and the CEO of the Sather Financial Group, a fee-only strategic planning and investment management firm.